Your savings may be funding factory farms

What do banks do with your money? How do banks make money? These are among the top banking questions people search for, and the answers are far more complex than you'd expect.

Banks make money primarily through lending: they take deposits, lend them out at higher interest rates, and keep the spread (more on that below). But this system has a hidden cost that most customers never discover. Between 2015 and 2022, six UK banks alone channelled £62 billion in deposits to industrial livestock companies - financing factory farm expansion while customers remained completely unaware.

Understanding how banks make money means understanding where your money goes. And that changes everything.

.jpeg)

How do banks make money? The spread, explained simply

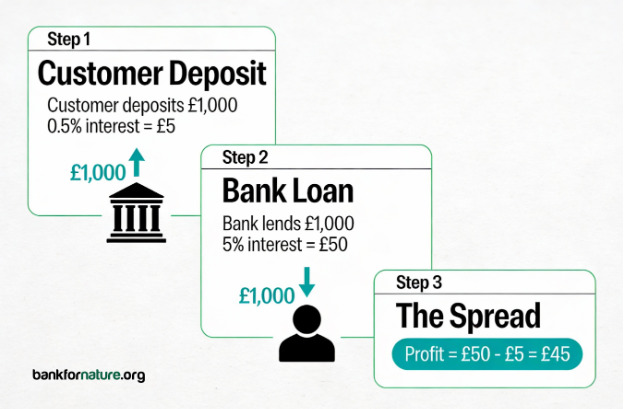

Banks are businesses designed to make profit, and they do it primarily through something called "the spread."

Here's how it works in three simple steps:

1. You deposit money. Let's say you put £1,000 into your current or savings account. The bank pays you a small amount of interest - perhaps 0.5% per year, or £5.

2. The bank lends your money out. That £1,000 doesn't sit idle in a vault with your name on it. Within days, the bank bundles your deposit with millions of others and lends it to businesses, homebuyers, or other borrowers at a much higher interest rate - say, 5% per year.

3. The bank keeps the difference. On your £1,000, the bank pays you £5 but earns £50 from the borrower. The £45 difference is their profit - this gap is "the spread," and it's how banks make most of their money.

This system is called fractional reserve banking. Banks are legally allowed to lend out approximately 95% of all deposits. Your money isn't actually reserved for you - it's working capital that banks use to generate returns.

Banks also make money from fees (overdraft charges, account maintenance, ATM fees) and from investing in securities, but the interest spread on loans is the foundation of retail banking.

So where do banks actually lend your money?

Now that we've answered "how do banks make money," the next question is: who are they lending to?

This is where things get uncomfortable for many banking customers - and where Bank for Nature's mission becomes crucial.

Banks don't just lend to small businesses and homebuyers. UK high street banks are among the world's biggest financiers of industrial animal agriculture - including factory farms that confine thousands of animals in intensive conditions, drive deforestation, and accelerate climate change.

The £62 billion link: UK banks and industrial livestock financing

Between 2015 and 2022, the UK's "Big Six" banks - Barclays, HSBC, Santander, Lloyds, NatWest, and Standard Chartered - provided at least £62 billion ($77 billion) in financing to 55 of the world's largest industrial livestock and animal feed companies.

That's not a typo. Sixty-two billion pounds from UK retail banks to factory farming corporations.

Here's how it breaks down:

.jpeg)

Additionally, these six banks owned nearly $1.2 billion in shareholdings in industrial livestock companies as of March 2023.

Which companies have been receiving this financing?

The financing flows to some of the world's most controversial industrial meat and dairy corporations. The top five recipients alone - JBS, Marfrig, Cargill, Tyson Foods, and Minerva - received a combined $21.6 billion between 2015 and 2022.

To put that in perspective: these five companies are collectively responsible for an estimated 595 million tonnes of greenhouse gas emissions every year - that's more than the entire annual emissions of the UK and Ireland combined.

A closer look: Barclays, JBS, and what the figures suggest

Let's make this concrete. Barclays has invested approximately £5 billion in JBS - the world's largest meat production company.

If you bank with Barclays, there's a strong chance some portion of your deposits is helping fund JBS operations. JBS owns several household UK brands you'd recognise:

- Moy Park (supplies roughly 25% of all processed chicken in UK supermarkets)

- Richmond sausages

- Pilgrim's UK (chicken products)

- Fridge Raiders (chicken snacks)

When you deposit money into your Barclays current account, a portion of it may be lent to JBS to expand their factory farming operations - operations that confine millions of chickens in industrial sheds, contribute to deforestation for animal feed production, and generate massive environmental costs.

But you didn't choose this. You also probably didn't even know it was happening. But through the mechanics of how banks make money - borrowing from depositors at low rates, lending to corporations at high rates - your everyday banking may fund that very industry.

The policy gap: why most banks have no factory farming exclusions

Of all of the banks featured on bankfornature.org, only a few have a position on factory farming.

This means most banks can, and do, invest customer deposits into factory farming projects that drive habit destruction, pollute our waterways and produce emissions, with no internal guidelines, risk assessments, or ethical guardrails.

Compare this to other sectors: most major banks now have detailed policies on fossil fuel financing, deforestation, and human rights. Yet factory farming remains a policy blind spot.

Why individual deposits have more impact than most customers realise

At this point, you might reasonably ask: "I'm just one person with a modest savings account. Does my money really make a difference?"

The answer is yes - for two critical reasons.

1. Banks Run on Deposits

Unlike most businesses, banks' core operations depend entirely on customer deposits. When deposit levels fall, banks lose their lending capacity. They cannot lend out money they don't have.

Every pound you withdraw and move to a more ethical bank is a pound that can no longer be lent to factory farming corporations. At scale, customer switching directly impacts what banks can and cannot finance.

2. Banks Are Watching Customer Sentiment

Financial institutions track customer feedback, complaints, and switching patterns obsessively. A 2024 survey found that 52% of banks now view environmental and climate issues as an emerging risk over the next five years - not because of regulatory pressure alone, but because customers are demanding change.

When customers leave a bank and publicly state factory farm finance as the reason, it creates reputational risk that boardrooms notice. It signals that this is a growing customer expectation, not a fringe concern.

En masse, these complaints get escalated, and that drives real change in what banks finance, whether that’s ditching harmful industries or investing in cleaner ones.

The Environmental and Financial Risks Are Real

This isn't just about ethics - it's about financial risk.

The World Economic Forum estimates that nature loss could reduce global GDP by up to $10 trillion by 2050. Banks financing factory farming are exposed to:

- Stranded assets as climate regulations tighten

- Default risk as industrial agriculture operations face rising costs and extreme weather

- Reputational damage as public awareness of factory farming impacts grows

- Regulatory scrutiny as governments mandate climate risk reporting.

In the UK, factory farming costs taxpayers over £1.2 billion annually through subsidies (£269 million) and pollution costs (£518 million) - costs that should be borne by producers but are instead put onto society.

Banks are lending to a sector with massive hidden liabilities and concentrated climate risk. For every pound banks lend to factory farming, they're taking on environmental, social, and financial risks that customers like you ultimately bear through financial system instability.

In 2016, the FAIRR Initiative identified at least 28 environmental, social, and governance (ESG) issues with the potential to significantly disrupt the global economy and erode the financial value of investments over both the short and long term.

Banks that have chosen to exclude factory farming

Not all banks finance factory farming. Some have explicitly excluded it:

The Co-operative Bank (UK)

The Co-operative Bank actively excludes factory farming from lending and scores highest (86%) in World Animal Protection's assessment of UK bank animal welfare policies.

Triodos Bank (UK & EU)

Triodos only finances organisations with positive environmental and social impact. It also scores highly on animal welfare policies, with an explicit exclusion on factory farming.

Atmos Financial (US)

This certified B Corporation digital bank exclusively finances climate-positive sectors including solar, electrification, and sustainable food systems, with zero factory farming investment.

Why plant-based food systems may represent a stronger financial bet

Here's what banks like these have figured out: excluding factory farming doesn't mean abandoning agricultural lending - it means redirecting capital toward a sustainable, fast-growing food sector.

The global plant-based food market is projected to grow from $30.4 billion in 2025 to $54.4 billion by 2032, expanding at 8.67% annually. In the first half of 2025 alone, alternative protein companies raised $443 million across 54 deals. Plant-based product categories are delivering strong returns: plant-based turnover surged 112% year-on-year for one major European food fund in 2024.

Unlike industrial animal agriculture, which faces mounting climate regulations, consumer backlash, and financial risks, plant-based food systems have aligned incentives. Consumer demand is accelerating, venture capital is flowing, and sustainability-linked lending allows banks to earn returns while financing the food transition and improving their sustainability performance.

Banks that exclude factory farming and invest in plant-based alternatives aren't making an ethical sacrifice. They're making a smart financial bet on the future.

Three steps you can take: check, message, and consider switching

The banking system's opacity means most customers have no idea their money finances factory farming. But now you know - and that knowledge comes with a choice.

Here are three actions you can take:

1. Check Your Bank

Start by understanding where your bank stands. Does it have a factory farming exclusion policy? Does it finance JBS, Cargill, or other industrial livestock companies?

Visit bankfornature.org to check your bank's profile. We've researched retail banks' factory farming exposure, ESG policies, and sustainability reports so you can see exactly where your bank stands.

2. Send Your Bank a Message

If your bank is financing factory farming, tell them you're concerned. Use Bank for Nature's free message tool to send a personalised email to your bank's leadership.

Banks monitor customer correspondence closely. Even a single message contributes to internal conversations about risk, reputation, and customer expectations.

3. Consider Switching

If your bank refuses to act, vote with your feet. While data on factory farming isn’t yet available, comparable data on fossil fuel finance is hopeful: switching to a bank that doesn’t fund this industry can reduce your money's carbon impact by up to 86%.

Bank for Nature makes it easy to find ethical banking alternatives.

Why this matters: deposits, accountability, and the power to push for change

Most people choose their bank based on convenience - branch location, app design, maybe interest rates. And then many don’t even think about what the bank does with deposits once they're in the account.

But how banks make money determines what gets built in the world. Every lending decision - every factory farm expansion, every industrial feedlot, every soybean crushing plant for animal feed - depends on bank financing.

When UK banks channelled $77 billion to industrial livestock companies between 2015 and 2022, they weren't making those decisions in a vacuum. They were using the deposits of millions of ordinary customers who never consented to fund factory farming.

You get to change that equation.

The banking system only works when customers trust it with their deposits. When customers move deposits to banks with better policies, the entire system responds. When customers publicly demand change, banks face reputational risk they cannot ignore.

Factory farming is one of the largest drivers of climate change, deforestation, biodiversity loss, water pollution, and animal suffering. It's also one of the most financially risky sectors banks lend to, with massive hidden costs and exposure to climate-related losses.

Your bank may be financing this system. But you don't have to be complicit.

Ready to check where your bank stands?

Ready to see where your bank stands?

- Check your bank on Bank for Nature – bankfornature.org

- Send your bank a message using their free tool on each bank page

- Explore ethical alternatives if it's time to switch

Start today. Your money, your choice.

What we've covered: key points

- Banks make money through "the spread" - paying depositors low interest, lending at high interest, keeping the difference.

- UK's six biggest banks provided £62 billion to factory farming companies (2015-2022).

- Barclays, HSBC, and Santander are the largest UK financiers of industrial livestock.

- Your deposits directly fund factory farm expansion through fractional reserve banking.

- Some banks (like The Co-operative Bank, Triodos and Atmos) are committed to not finance factory farming.

- Switching banks or sending messages creates real pressure for change.

- Bank for Nature helps you check your bank, message their leadership, and find an alternative.

Stand Against Nutrition Misinformation

Misinformation is a growing threat to our health and planet. At foodfacts.org, we're dedicated to exposing the truth behind misleading food narratives. But we can't do it without your support.

References

- Foodrise, 2023, Bankrolling the Butchers: The role of UK banks in financing industrial meat and dairy corporations - https://foodrise.org.uk/wp-content/uploads/2023/11/Feedback-2023-Bankrolling-the-Butchers-report.pdf

- Corporate Finance Institute, 2020, How Do Banks Make Money? - https://corporatefinanceinstitute.com/resources/economics/how-do-banks-make-money/

- Investopedia, 2025, Understanding Fractional Reserve Banking: How It Fuels Economic Growth - https://www.investopedia.com/terms/f/fractionalreservebanking.asp

- Banks.com, 2025, Where Do Banks Put Their Money? - https://www.banks.com/articles/banking/where-banks-put-money/

- State of Connecticut Department of Banking, Undated, ABC’s of Banking - https://portal.ct.gov/dob/consumer/consumer-education/abcs-of-banking---banks-and-our-economy

- World Animal Protection, 2025, Barclays is funding horrifying animal cruelty through £5bn JBS investment - https://www.worldanimalprotection.org.uk/latest/news/barclays-funding-factory-farming/

- Bank for Nature, 2026, Home: Discover Nature-Friendly & Ethical Banks - http://bankfornature.org

- Brite, 2025, 5 Critical Consumer Lending Trends 2024 - https://britepayments.com/resources/article/5-essential-consumer-lending-trends-2024/#elementor-toc__heading-anchor-3

- Bank for Nature, 2026, About Bank for Nature - https://bankfornature.org/about

- Friends of the Earth, 2025, Industrial Livestock Production: Climate-Related Financial Risks - https://foe.org/resources/industrial-livestock-production-climate-related-financial-risks/

- FAIRR Initiative, 2016, Factory Farming: Assessing Investment Risks - https://www.fairr.org/resources/reports/factory-farming-assessing-investment-risks

- Bank for Nature, 2026, The Co-operative Bank - https://bankfornature.org/banks/the-co-operative-bank

- Bank for Nature, 2026, Triodos Bank - https://bankfornature.org/banks/triodos-bank

- Plant Based News, These UK Banks Have The ‘Worst Animal Welfare Policies,’ Says Study - https://plantbasednews.org/culture/ethics/uk-banks-animal-welfare-policies/

- Bank for Nature, 2026, Atmos Financial - https://bankfornature.org/banks/atmos-financial

- MMR Statistics, 2026, Global Plant-Based Food Market Size (2025) & Forecast (2026–2032) - https://www.mmrstatistics.com/reports/930054/global-plant-based-food-market

- Cultivated X, 2025, Investments in Alternative Proteins Total $443 Million in First Half of 2025 - https://cultivated-x.com/investments-finance/investments-alternative-proteins-total-443-million-first-half-2025/

- Triodos Investment Management, 2025, Investing in healthy and sustainable food - https://www.triodos-im.com/binaries/content/assets/shared/fund-assets/tftef/triodos-food-transition-europe-fund-impact-report-2024.pdf

- The Co-operative Bank, 2025, Consumers warned by the first fossil-free certified bank that who they choose to bank with matters - https://www.co-operativebank.co.uk/about-us/press-release/2025/consumers-warned-by-the-first-fossil-free-certified-bank-that-who-they-choose-to-bank-with-matters/

foodfacts.org is an independent non-profit fact-checking platform dedicated to exposing misinformation in the food industry. We provide transparent, science-based insights on nutrition, health, and environmental impacts, empowering consumers to make informed choices for a healthier society and planet.

.svg)